NMHC Top 50 Rankings Just Dropped — Here’s What the Data Really Reveals About Multifamily Power Players

Based on research and analysis by Jay Parsons, Rental Housing Economist (Apartments, SFR), Speaker and Author

The latest National Multifamily Housing Council Top 50 rankings are out—and at first glance, it looks like a leaderboard of giants.

But look closer… and the real story is far more disruptive.

This isn’t an industry dominated by titans.

It’s one of the most fragmented, competitive, and opportunity-rich sectors in the U.S. economy.

Here’s what actually stands out—and why it matters for owners, operators, and investors trying to protect NOI and scale smarter.

1) The “Biggest Player” Barely Moves the Needle

Let’s start with the biggest name in multifamily: Greystar.

Ownership market share: < 0.5%

Management market share: ~4%

Construction starts: ~2%

And that’s the #1 ranked firm across multiple categories.

👉 Let that sink in.

There are virtually no true “behemoths” in this industry. Compared to sectors like tech, retail, or airlines—where top players dominate—multifamily remains wildly decentralized.

Why it matters:

Competitive pressure stays high

Innovation isn’t dictated by a few players

Operators must differentiate at the property level—not rely on brand dominance

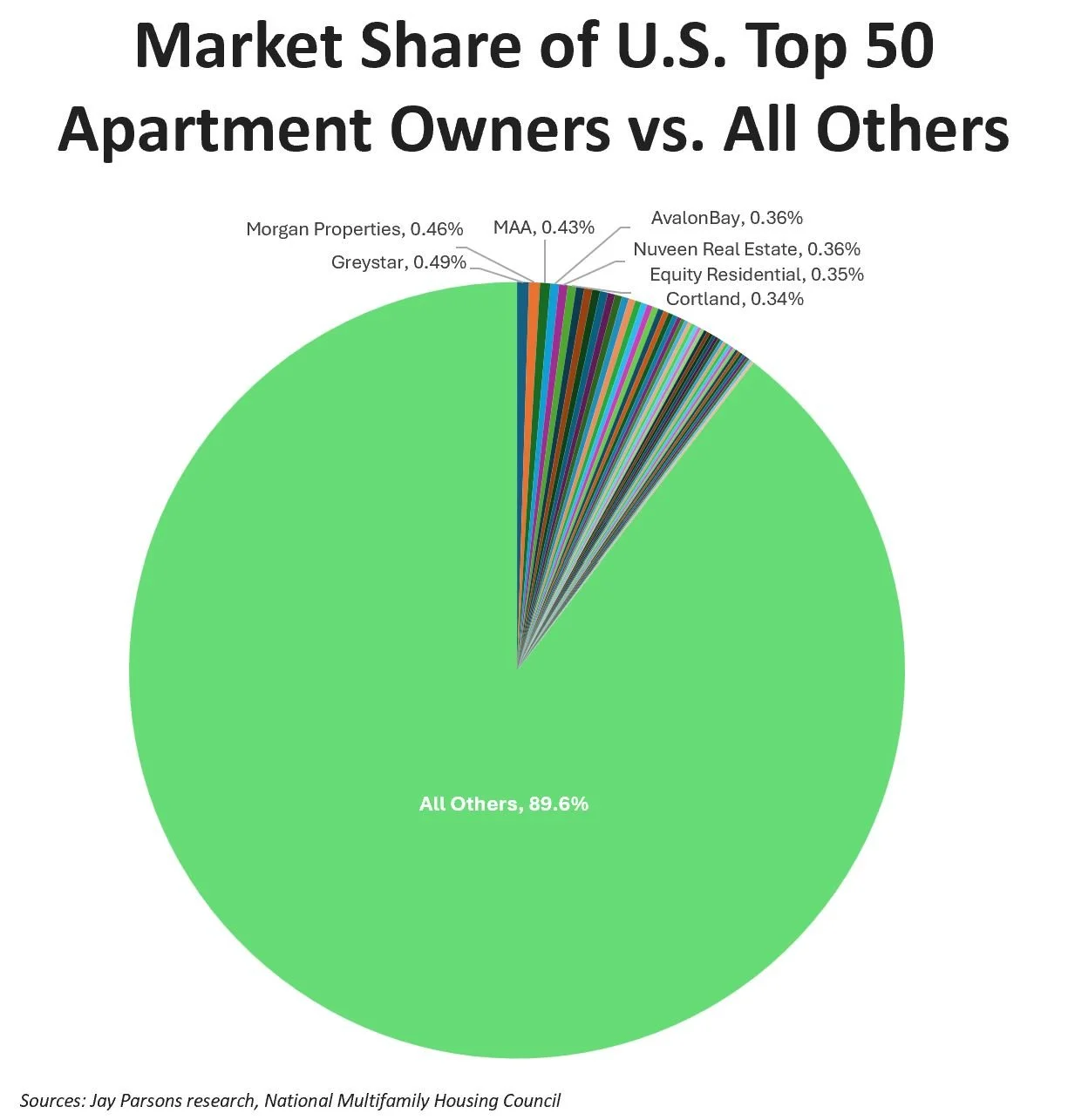

2) Ownership Is Fragmented—And Getting More So

Even at the very top, fragmentation is accelerating.

The Top 50 owners combined control just 11% of total units

In 2015:

8 owners had 100K+ units

The largest held 244K units

Only 3 owners exceed 100K units

The largest holds just 119K units

Meanwhile, Morgan Properties just entered the 100K club—adding 13,700 units.

So… why is ownership so fragmented?

Highly liquid transaction market

Low operational barriers (if capital is available)

Ability to outsource management to third-party firms

Bottom line:

Anyone with capital can enter—and scale—without building a full operational platform.

3) Big Developers Are Quietly Pulling Ahead

Development activity didn’t spike dramatically year-over-year—but something more subtle happened:

Top developers got busier.

What this signals:

Larger developers are leveraging:

Cheaper capital access

Operational efficiencies

Stronger pipelines

Meanwhile, smaller developers are facing tighter constraints.

Translation: Scale is starting to matter more—but only in development.

4) Management Is Where Consolidation Is Actually Happening

While ownership is fragmented, management is consolidating fast.

Top 50 managers now oversee ~5.3 million units

That’s a 6% YoY increase—likely a record

Why?

Margin compression is real

Cost pressures are rising

Larger operators deliver:

Better economies of scale

More efficient systems + staffing models

Key takeaway:

If you’re not scaling operations, you’re likely losing margin.

5) The Race for Scale: Who’s Winning in Management?

Greystar surpasses 1 million units managed

Asset Living adds 158K units, holding #2 with 446,427 units

Growth fueled by acquiring FPI Management

Other notable growers:

Arqline

ZRS Management

Each added ~20K+ units.

The pattern is clear:

Management is becoming a scale game

Ownership is still a fragmentation game

What This Means for Your NOI (And Why Most Operators Miss It)

This is where most people misread the data.

They focus on rankings.

They miss the operational implication:

In a fragmented ownership landscape, property-level performance is everything.

You’re not competing with Greystar.

You’re competing with the property down the street.

⚠️ The Hidden Risk in a Fragmented Industry

Fragmentation creates opportunity—but also risk:

Inconsistent operations

Inefficient labor allocation

Rising compliance complexity

Margin leakage across portfolios

And in a thin-margin environment, small inefficiencies compound fast.

🚀 The Operators Who Win in This Market Do One Thing Differently

They standardize and scale operational efficiency, not just acquisitions.

That means:

Reducing onsite labor drag

Streamlining waste + recycling logistics

Improving resident experience (without increasing headcount)

Protecting NOI through operational discipline

Review our 2026 Multifamily Outlook

Final Takeaway (From Jay Parsons’ Data)

The NMHC Top 50 data tells a very clear story:

Ownership = fragmented

Management = consolidating

Development = scaling advantage

Margins = under pressure

The winners won’t just be the biggest.

They’ll be the most operationally efficient.

Want to Compete Like the Top Operators?

If scale and efficiency are defining the winners…

Then your property-level operations need to evolve.