By Les Leith, CEO & COO at National Doorstep Pickup

The apartment market just got a new warning signal.

It is not that renters have stopped moving altogether.

It is that they are moving differently.

For apartment owners, regional managers, and property managers, this matters because the old leasing playbook was built around a more mobile renter. A renter who would cross markets for lifestyle, job growth, rent savings, or a better amenity package.

In 2026, that renter still exists.

But there are fewer of them.

And that means the communities that win are not just the ones chasing new traffic. They are the ones keeping current residents, reducing daily friction, improving resident convenience, and giving local movers a reason to choose them over the property down the street.

The Big Shift: Fewer Moves, More Local Decisions

That is a major signal for multifamily leasing teams.

When renters stay in the same city, they usually already know the neighborhood, the commute, the rent range, the traffic patterns, the grocery stores, the school zones, the entertainment districts, and the pain points.

They are not just shopping for a city.

They are comparing properties.

That makes the competitive set tighter.

A renter moving from one apartment community to another inside the same metro is likely comparing:

Monthly rent.

Concessions.

Parking.

Package handling.

Trash and recycling convenience.

Cleanliness.

Safety perception.

Maintenance responsiveness.

Amenity value.

Online reputation.

Resident experience.

In other words, the decision becomes less about the city and more about the property.

That is where operational execution becomes a leasing advantage.

A clean community, reliable service, strong curb appeal, easy waste disposal, and visible resident convenience can influence which apartment community wins the lease — and which one keeps the resident at renewal.

The New Renter Reality: Moving Less Does Not Mean Demand Is Gone

The 2026 mobility story is not a “no one is moving” story.

It is a “renters are being more selective” story.

People are still changing apartments. They are still looking for better value. They are still relocating for jobs, affordability, lifestyle, family, and quality of life. But they are doing it more carefully, more locally, and often with more price sensitivity.

For multifamily operators, that changes the math.

When fewer renters are making long-distance moves, properties cannot depend as heavily on broad migration momentum to fill units. Local traffic becomes more important. Renewal strategy becomes more important. Resident satisfaction becomes more important.

And every controllable service matters more.

In a market where renters are staying put, a renewal is not just a signed lease.

It is NOI protection.

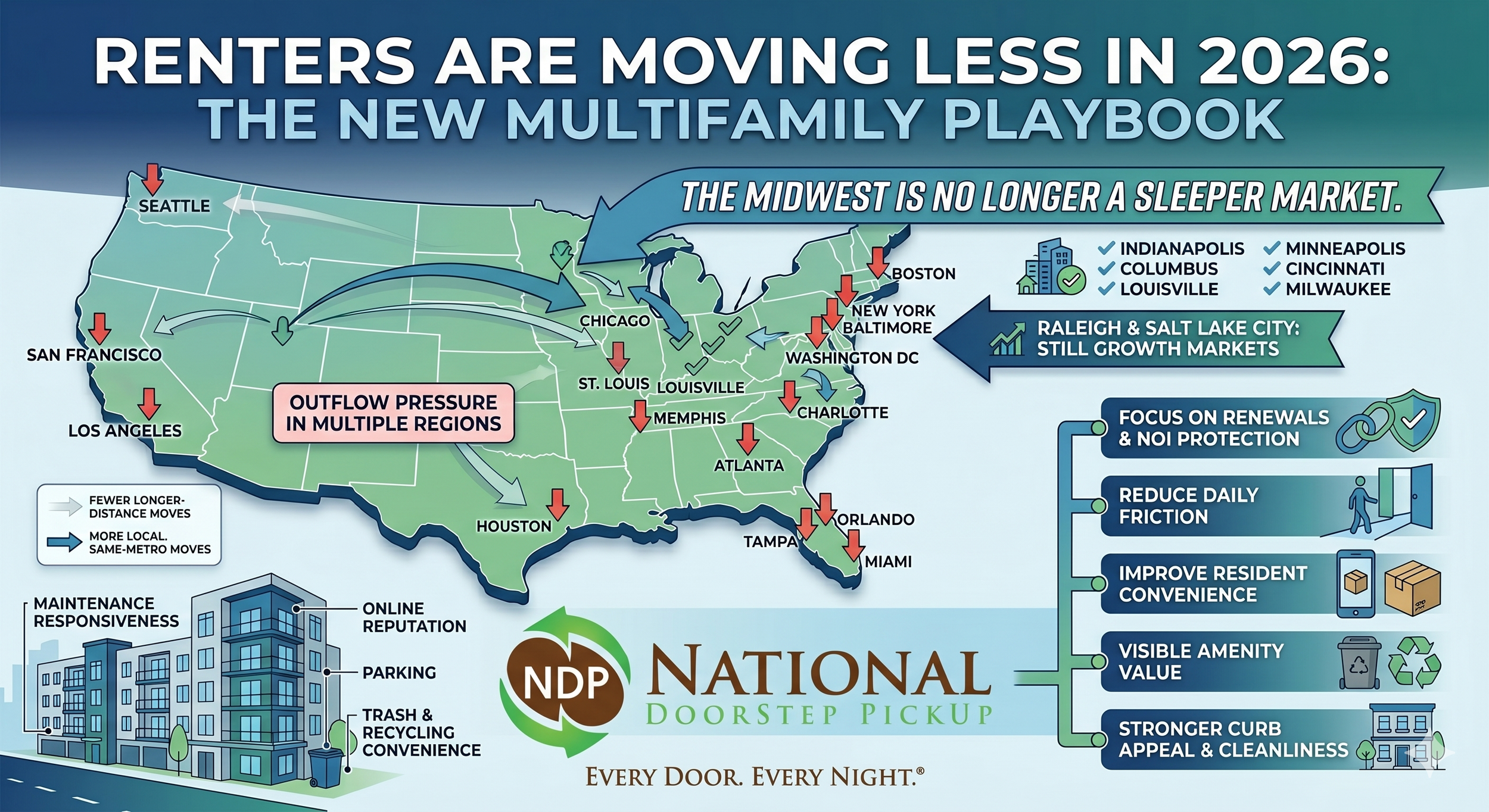

Exhibit 3: The Midwest Is No Longer a Sleeper Market

One of the biggest takeaways from Bank of America Institute’s data is that the Midwest is outperforming expectations.

That is a major shift in the multifamily conversation.

For years, apartment industry growth headlines focused heavily on the Sun Belt. Markets like Austin, Dallas, Phoenix, Tampa, Orlando, Miami, Nashville, Raleigh, and Charlotte dominated the migration and construction conversation.

But Exhibit 3 shows that the Midwest is punching above its weight.

Why does that matter?

Because many Midwest metros offer something renters are actively looking for in 2026: relative affordability, job access, livability, and a lower cost of entry compared with expensive coastal markets and oversupplied Sun Belt metros.

Indianapolis and Columbus are especially important because they combine population inflow with practical affordability. These are not just lifestyle relocation markets. They are value-driven apartment markets where renters may be looking for a better balance between rent, wages, space, commute, and quality of life.

For apartment owners, this creates a clear takeaway:

The next wave of multifamily opportunity may not only come from the loudest growth markets. It may come from steady, operationally disciplined markets where renter demand is supported by affordability and local economic stability.

This is also where resident experience becomes a competitive edge.

In markets where renters are staying local or moving from nearby areas, they already know the neighborhood. They are comparing one property against another. A clean community, reliable trash pickup, strong curb appeal, convenient recycling, and a professionally managed resident experience can influence which property wins the lease.

In other words, the Midwest migration story is not just about population growth.

It is about local competition.

Salt Lake City and Raleigh Are Still Growth Markets to Watch

The Midwest was a standout, but it was not the only region attracting movers.

Salt Lake City ranked among the strongest growth markets, and Raleigh continued to show strong population momentum. These markets remain important because they reflect a different part of the migration story: renters are still willing to relocate when the value proposition is strong enough.

Salt Lake City offers access to jobs, outdoor lifestyle, and regional growth.

Raleigh continues to benefit from education, technology, healthcare, and quality-of-life demand.

But even in attractive growth markets, operators should be careful.

Population inflow is not the same thing as unlimited rent growth.

When new supply gives renters more choices, the renter has more leverage. When incoming residents skew younger or lower income, they may prioritize affordability over premium finishes or high-end amenity packages.

That is why growth markets still need disciplined operations.

Traffic alone is not enough.

Exhibit 4: Outflow Markets Show Where the Pressure Is Building

Exhibit 4 tells the other side of the migration story.

Memphis and Washington, DC led the major metros with year-over-year domestic population declines. Other outflow markets included Los Angeles, Miami, Boston, Orlando, San Jose, New York, Baltimore, St. Louis, Seattle, San Francisco, Houston, Tampa, Atlanta, Chicago, Charlotte, and others.

That list matters because it cuts across multiple regions.

This is not just a coastal problem.

It is not just a Sun Belt problem.

It is not just a Northeast problem.

The outflow map shows that renter behavior is becoming more selective.

Some renters are leaving high-cost coastal metros. Others are leaving markets where affordability has weakened. Some may be moving out of metros with heavy supply pressure. Others may be choosing nearby suburbs, exurbs, or lower-cost regions where their income stretches further.

For multifamily operators, outflow markets require a different strategy.

When a metro is losing residents, leasing teams cannot rely on broad population growth to fill the funnel. Properties need sharper positioning, stronger renewal strategy, better service consistency, and better day-to-day resident satisfaction.

Every operational problem becomes more expensive because the replacement renter may be harder to find.

That is especially true in competitive submarkets where multiple communities are chasing the same local renter.

If a resident is already questioning the value of their rent, small frustrations can become renewal killers. Overflowing dumpsters, inconsistent trash service, poor recycling access, hallway odors, missed pickups, messy breezeways, and weak curb appeal can become the final reason a resident decides to leave.

In a slower mobility market, resident retention is no longer a soft metric.

It is an NOI protection strategy.

The more difficult it becomes to attract replacement residents, the more valuable it becomes to keep the residents already in place.

Why the Outflow Markets Are a Warning for Property Managers

The outflow markets in Exhibit 4 should not be read as “bad markets.”

Many of these metros are still large, economically important apartment markets. New York, Boston, Los Angeles, Miami, Orlando, Houston, Tampa, Atlanta, Seattle, and San Francisco are not disappearing as renter markets.

But they are becoming more complicated.

A property can be located in a high-demand metro and still face pressure from declining domestic migration, elevated concessions, new supply, affordability fatigue, or changing renter demographics.

That means owners and managers should be watching more than occupancy.

They should be watching:

Resident renewal behavior.

Concession levels.

Traffic quality.

Application-to-lease conversion.

Move-out reasons.

Trash and cleanliness complaints.

Online reviews.

Amenity utilization.

Local competitor pricing.

Service consistency.

The best operators will not wait until occupancy drops to respond.

They will tighten operations before the market forces them to.

Exhibit 9: Rent Growth Is Not Following Migration in a Straight Line

Exhibit 9 adds the most important rent-growth nuance.

Median rental payments were rising year-over-year in Minneapolis, Seattle, and New York, while declining in Austin, Denver, and Miami.

That is a powerful signal because it shows that population inflow does not automatically equal rent growth.

Austin and Denver, for example, have been among the markets attracting renter inflows, but Bank of America’s data shows negative year-over-year rental payment growth. That suggests renters may be moving in, but they are not necessarily paying more.

They may be trading down.

They may be choosing smaller units.

They may be taking advantage of concessions.

They may be moving farther from the urban core.

They may be selecting communities with fewer premium features.

They may be doubling up with roommates.

They may be prioritizing affordability over amenity packages.

This is where oversupply matters.

When renters have more options, they have more leverage. They can shop harder. They can compare concessions. They can choose newer supply with better specials. They can move into a less expensive submarket. They can push back on pricing.

That is why a market can show renter demand and still experience rent-payment weakness.

Minneapolis tells a different story. It showed renter inflow and rising rental payments, which may indicate a healthier balance between demand and available supply. It may also suggest that renters have fewer opportunities to trade down compared with some Sun Belt and Western markets where new supply has expanded options.

The lesson is simple:

Rent growth depends on the relationship between demand and supply, not demand alone.

Strong Inflows Do Not Always Mean Stronger Rent Payments

This is one of the most important takeaways for multifamily owners in 2026.

A market can attract renters and still have flat or declining rental payments.

That sounds contradictory at first. If people are moving in, shouldn’t rents rise?

Not always.

Bank of America’s data points to two major reasons: oversupply and renter demographics.

In several markets, new apartment supply gives renters more choices. When renters have more choices, they can trade down, negotiate, take concessions, choose smaller units, move farther out, or pick communities with fewer premium features.

The second factor is who is moving.

New arrivals in some growth markets skew younger and lower income. These renters are more likely to be price-sensitive and more likely to search for the cheapest acceptable housing option.

That means demand can be real while pricing power stays limited.

For owners and managers, this is the operating reality of 2026:

More traffic does not automatically equal stronger rent growth.

More applications do not automatically equal higher effective rent.

More move-ins do not automatically equal better NOI.

The quality of demand matters. The supply picture matters. The resident experience matters. And controllable operational value matters.

What This Means for Apartment Owners and Property Managers

The 2026 mobility trend creates a more competitive, retention-driven apartment market.

When renters are moving less, every renewal matters more.

When local moves dominate, nearby properties become direct threats.

When rent payments soften, operators need to protect NOI without depending entirely on rent growth.

That is why value-based amenities are becoming more important.

Renters may push back on higher base rent, but they still care deeply about convenience, cleanliness, safety perception, and daily quality of life. The communities that can deliver visible service value have a stronger chance of defending retention and standing out in local searches.

This is especially true for services residents experience every week — and in many cases, every night.

Trash and recycling are not glamorous.

But they are highly visible.

Overflowing dumpsters, hallway odors, missed pickups, stained breezeways, and confusing recycling areas can quickly damage a property’s reputation.

In a market where renters are comparing communities across the same neighborhood, that matters.

The Multifamily Takeaway: Traffic Is Not Enough

For apartment operators, these migration and rent-payment trends should change how 2026 performance is evaluated.

A market with inflows may still have weak effective rent growth.

A market with outflows may still have strong submarkets.

A market with high demand may still require concessions.

A market with rent growth may still be vulnerable if resident experience is poor.

This is why property-level execution matters.

Owners and managers cannot control national migration patterns. They cannot control interest rates, new construction deliveries, or renter income trends.

But they can control the daily resident experience.

They can control cleanliness.

They can control service consistency.

They can control common-area presentation.

They can control waste management.

They can control how easy or frustrating it is to live at the property.

That matters in a market where renters are moving less, staying local, and comparing communities more carefully.

Why Valet Trash and Doorstep Recycling Fit the 2026 Market

A professionally managed doorstep waste and recycling program gives apartment communities a practical way to compete on convenience without relying only on rent discounts.

For residents, it removes a daily hassle.

For property teams, it helps reduce trash-area pressure, supports cleaner common areas, improves curb appeal, and creates a service touchpoint residents can actually see.

For owners, it can help convert a routine operational need into a resident-facing amenity.

That is the sweet spot in a softer rent-growth environment: services that improve resident experience while supporting property operations.

National Doorstep Pickup helps apartment communities deliver consistent valet trash and doorstep recycling programs designed around the realities of multifamily operations. From garden-style communities to mid-rise buildings, urban properties, student housing, senior living, and mixed-use communities, the goal is simple:

Cleaner communities.

Better resident convenience.

Fewer waste-management headaches for onsite teams.

Stronger resident retention.

Better operational consistency.

The New Leasing Message: Make Staying Easier

If renters are moving less, the biggest opportunity may not be only in attracting new residents.

It may be in giving current residents fewer reasons to leave.

That means property managers should be asking:

Are we making daily life easier for residents?

Are we reducing common complaints?

Are our amenities visible and valuable?

Are we protecting cleanliness and curb appeal?

Are we helping residents feel that the community is professionally managed?

Are we giving local renters a reason to choose us over the community nearby?

Are we creating a better renewal conversation?

Are we protecting NOI with operational consistency?

In 2026, the best leasing strategy may also be a retention strategy.

Markets to Watch in 2026

Based on the Bank of America migration patterns, apartment operators should pay close attention to markets showing strong renter or population momentum, including:

But operators should also be careful not to confuse inflow with automatic rent strength. In supply-heavy markets, especially parts of the South and West, renters may have more leverage and more ability to trade down.

That makes service differentiation even more important.

The Bottom Line for Multifamily in 2026

The renter is not gone.

The renter is more selective.

People are moving less. When they do move, they are often staying local. The Midwest is gaining strength. Salt Lake City and Raleigh are still attracting new residents. Some major coastal hubs and Sun Belt metros are still seeing outflows. And in several high-demand markets, rental payments are softening because supply and renter demographics are changing the economics.

For multifamily owners and property managers, this is the moment to focus on what can be controlled:

Resident retention.

Operational consistency.

Cleanliness.

Convenience.

Amenity value.

NOI protection.

In a slower mobility market, the communities that win will not simply be the ones with the biggest concession.

They will be the ones that make residents think twice before moving at all.

National Doorstep Pickup helps apartment communities turn waste collection and recycling into a cleaner, more convenient resident amenity — delivered consistently, professionally, and with accountability.

Every Door. Every Night.®